Account Freezing Orders jump more than 170% in three years as HMRC cracks down on suspected criminal activity

Following the dumping of sewage into our waterways, a case against six UK water companies begins on Monday (September 23, 2024).

- Account Freezing Orders and Forfeiture Orders see dramatic rise over three-year period

- Low evidential threshold makes widespread use concerning, warns RPC

- £14.5mn of assets returned in last financial year

HMRC has dramatically increased its use of Account Freezing Orders (AFOs) and Forfeiture Orders (FOs) in the last three years as part of its crack-down on suspected criminal behaviour, according to a Freedom of Information request by international law firm, RPC.

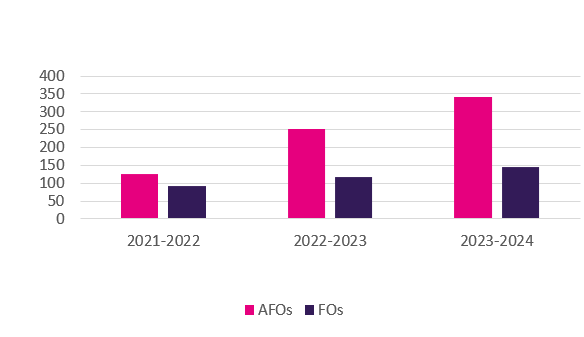

According to data revealed by the Freedom of Information request, the number of AFOs has risen from 125 in the 2021/2022 financial year to 252 in 2022/2023, and has increased to 341 in 2023/2024, representing an increase of more than 170% over a three-year period. Additionally, the value of assets frozen by AFOs has increased from £43mn in 2021/2022 to £57m in 2023/24.

The number of Forfeiture Orders has also increased over the same period, rising from 92 in 2021/2022 to 144 in 2023/2024, when the total value of assets seized was close to £23m.

AFOs were introduced under the Criminal Finances Act 2017 and allow a court to order bank accounts to be frozen for up to two years while law enforcement agencies investigate the source of funds and prevent disposal.

AFOs are granted by the Magistrates Court, and do not require authorisation by a senior judge, or indeed a qualified lawyer. The threshold is low. Rather than proving criminality to the usual standard of beyond reasonable doubt, the relevant law enforcement agency only needs to prove its case on a balance of probabilities. AFOs can apply to accounts with balances over £1,000 and enable authorities to preserve funds for subsequent forfeiture.

The low evidential threshold for obtaining an AFO means that this rise in their use is potentially concerning, argues Adam Craggs, Partner and Head of Tax Disputes at RPC. “Since their introduction, we have seen HMRC invoking these powers on an increasingly regular basis, even though we know that in many cases they do not lead to a subsequent successful forfeiture of assets or criminal prosecution. While money can be returned, this is of little consolation for the individuals and businesses that see their operations unduly impacted as a consequence of their funds being frozen.”

Not all AFOs will result in a forfeiture, which occurs only when the court is satisfied that the moneys seized are the proceeds of crime or used to facilitate a crime. In the 2023/2024 financial year, £14.5m of assets were returned, relating to 75 AFOs.

Michelle Sloane, Partner at RPC added: “As AFOs and FOs become more frequent, it is critical that individuals and businesses are aware of their rights and how to successfully challenge them. Those affected should immediately contact a specialist solicitor, who will be able to advise on appropriate next steps to minimise disruption to their lives and business operations.”

Stay connected and subscribe to our latest insights and views

Subscribe Here